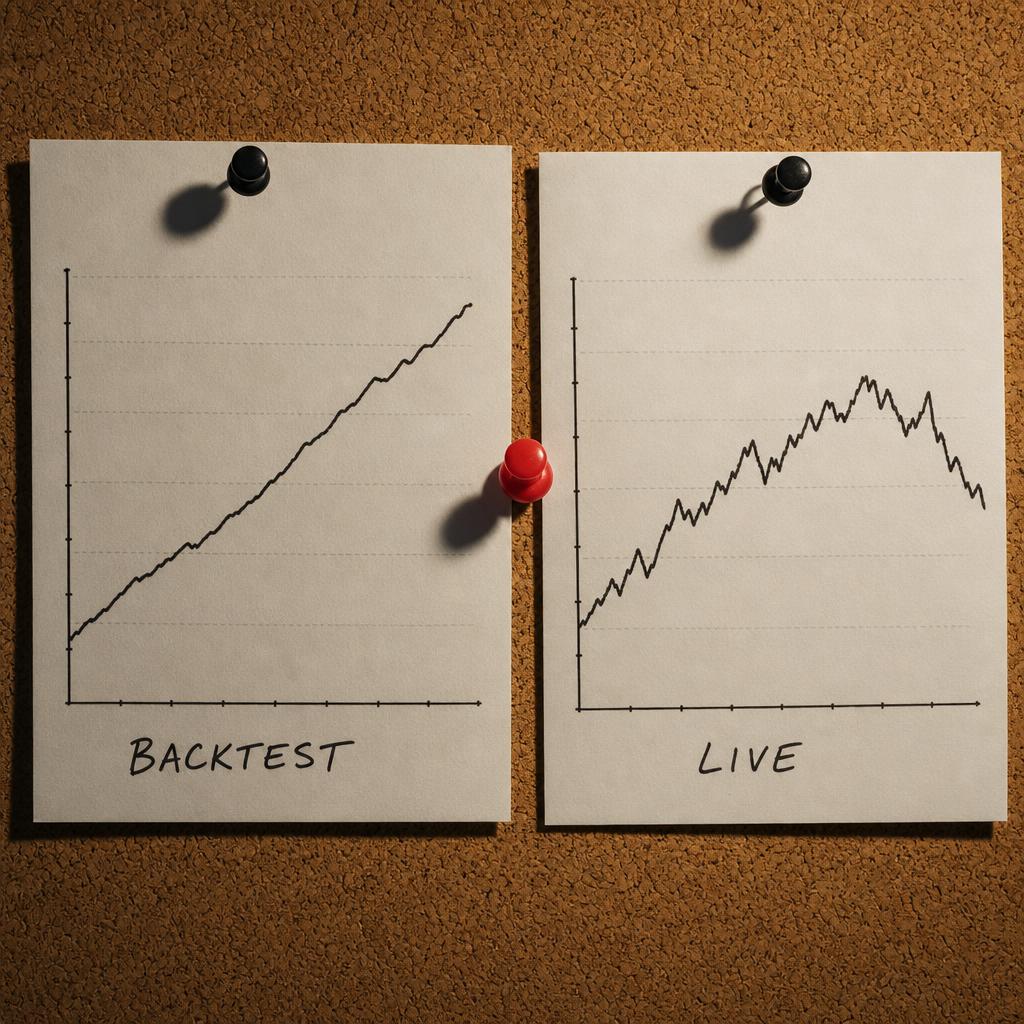

The pitch is always the same. A YouTube thumbnail with a green equity curve climbing through three years of historical data. "This AI trading bot returned 47% annualized in backtests." The bot goes live in February. By April, the same trader is filming a different video — about why they think the strategy needs a few weeks to "adjust to market conditions." By July, the channel is posting about a new bot.

The backtest-to-live gap is one of the most consistent failure modes in retail algorithmic trading. And it's almost never the strategy. It's six specific things that backtests can't simulate, and that production trading systems have to address explicitly.

What the backtest is actually measuring

A backtest replays historical price data through your strategy's logic and computes what would have happened if the bot had been live. That sentence does a lot of work, and most of the gap between backtest and live happens inside that sentence.

The first lie is price data. The backtest's "price" is usually one of: the closing price of a bar, the midpoint between bid and ask, or a single tick. Live trading never gives you that price. You pay the ask when you buy and receive the bid when you sell. The spread is real money. On a 1.0850 EUR/USD entry with a 0.7 pip spread, you've already lost $7 per standard lot before your bot has done anything. Over 200 trades a month, the spread eats more than most retail traders' alpha.

The second lie is fills. Backtests assume you got the price you wanted. Live trading on retail brokers often gives you slippage — sometimes a fraction of a pip, sometimes (during news) entire pips. Stops trigger at price levels that don't match where you placed them. Limit orders sometimes don't fill at all.

The third lie is spread variation. Most backtests use a fixed spread. Real spreads widen during low-liquidity hours (Asian session for some pairs, weekends for crypto) and explode during news. A 0.7 pip backtested spread becomes a 4.2 pip live spread at FOMC.

The fourth lie is latency. Your signal computes, your order goes to the broker, the broker routes to a liquidity provider, the LP either matches or rejects. By the time you have a fill, the market has moved. On a momentum strategy this hurts; on a mean-reversion strategy it sometimes helps; either way the backtest didn't model it.

The fifth lie is adversarial market makers. Several retail brokers run the other side of your trade. When your bot enters a position, the broker has an incentive to give you the worst execution within their compliance window. This is not paranoid — it's documented in CFTC and FINRA actions across the past decade. Backtests on historical price feeds don't capture it.

The sixth lie is your psychology. The backtest assumes the bot ran for three years without intervention. In live trading, the bot ran for 11 days before you turned it off for "just one news event" and forgot to turn it back on for 17 hours.

What survives the live gap

The good news: each of those six gaps is addressable. Production trading systems address them explicitly. Most retail builds don't, which is why most retail bots die in month one.

Spread modeling. Your backtest should use the worst historical spread for the relevant hour, not the average. If your strategy doesn't survive that, it's an idealization, not a system.

Slippage budget. Every trade should assume a slippage cost on entry and exit. Real slippage on retail brokers ranges from 0.2 pips on a major pair in London session to 3+ pips during news. Bake the expected slippage into your stop and take-profit math.

News window filtering. Major scheduled news (NFP, FOMC, CPI, ECB) creates pricing anomalies that destroy strategies built for normal regimes. The cheap fix: stop entering new positions 15 minutes before and 30 minutes after major releases. The expensive fix: a regime-classifier that knows when "normal" pricing breaks down.

Broker latency benchmarking. Run a measurement script that timestamps signal generation, order send, and fill receipt. Real retail latencies on commodity brokers range from 50ms (good) to 400ms (terrible). Strategies with edges measured in fractions of a pip require sub-100ms latency. Most retail traders never measure this.

Execution venue selection. For Forex, ECN brokers (where you trade against liquidity providers) systematically outperform market-maker brokers for serious algorithmic strategies. The cost is wider commissions; the gain is honest fills.

Human-out-of-the-loop architecture. Once the bot is configured and the kill-switch is set, the human shouldn't be making real-time decisions. That's where the seventh failure mode lives — the trader overriding the bot during drawdown because they "see what's happening." If your system requires you to not intervene during a $4K losing week, it's not a system; it's a willpower test.

Show the mechanism

Here's what a production-grade AI trading bot's pre-trade check actually does, in concrete terms:

On signal generated:

1. Check current spread for symbol (reject if > 2x median)

2. Check time-to-next-scheduled-news (reject if within ±15 min window)

3. Check current liquidity tier (reject if Asian session for certain pairs)

4. Check account drawdown state (reject or downsize based on mode)

5. Check correlated open positions (reject if portfolio risk exceeds cap)

6. Compute size based on volatility (ATR-based, not fixed lot)

7. Place order with broker

8. Compare fill price vs signal price (log slippage; alert if > threshold)

Eight independent gates. Each one rejects a class of trade that backtests said would be profitable but live trading would punish. Strategies that survive these gates are dramatically slower to enter positions — and dramatically more likely to be profitable when they do.

Smart money concepts (SMC) and Inner Circle Trader (ICT) methodology don't replace these gates. They inform what signals get generated in the first place — by identifying institutional order blocks, fair value gaps, and liquidity sweeps. But signal generation is upstream of execution. SMC tells you where the smart money is positioned; the execution architecture decides whether to take the trade given the live market conditions.

Who should care

- Anyone who's bought, built, or backtested an AI trading bot: the backtest is the easy part. The execution architecture is where the next six months of work lives.

- Builders considering shipping a trading bot product: if your product's marketing leans on backtest results, you have an honesty problem. Backtests are necessary but they're not the claim that matters.

- Retail traders deciding between bots: the questions to ask the vendor are "what's your slippage model" and "show me three months of live equity, not backtested." If they can't answer, walk.

The bots that don't break in live aren't the ones with the prettiest backtests. They're the ones whose builders modeled the six lies into the architecture before going live.

If you're looking for a trading system that's been built around these failure modes from the start — multi-agent risk validation, regime-aware mode switching, ICT-first market structure, honest live performance reporting — that's exactly what FlowiAI Trader is. The strategy layer is one input. The execution architecture is the system.